For many used car dealers Autotrader has always been a necessary cost of doing business. It is where the eyeballs are, and it is where the leads come from. But over the last few years something has changed. Dealers with 30 to 50+ cars in stock are finding their monthly Autotrader bills creeping into the thousands. Mid-sized independents are reporting four figure contracts as standard, and larger groups are routinely into the tens of thousands every month.

At the same time lead volumes have not kept pace with rising costs. New mandatory features like the Deal Builder workflow and compulsory login before an enquiry have caused frustration across the dealer community. Conversations in trade groups and forums show a clear trend. Dealers are asking a simple question. Is there another way?

The answer is yes. Not by moving to another marketplace, but by building a customer acquisition engine that you control.

At the same time lead volumes have not kept pace with rising costs. New mandatory features like the Deal Builder workflow and compulsory login before an enquiry have caused frustration across the dealer community. Conversations in trade groups and forums show a clear trend. Dealers are asking a simple question. Is there another way?

The answer is yes. Not by moving to another marketplace, but by building a customer acquisition engine that you control.

How Much Autotrader Really Costs In 2025

Autotrader do not publish a fixed price list for their dealer packages. Instead you are quoted based on stock levels, package tier and the number of additional tools you bolt on. Their own financial results, however, give a much clearer picture of what dealers actually pay.

Autotrader Group plc report an Average Revenue Per Retailer (ARPR) of £2,994 per month in their latest half year results. A year earlier it was £2,721. Over the last several years ARPR has risen consistently as the company uses what it calls price and product levers to drive growth. For dealers this simply means annual uplifts and increased pressure to adopt additional services.

Independent dealers with around 50 cars regularly report monthly invoices of £3,000 to £4,000. In one well known dealer group a site shared that they pay £3,500 for 50 cars. Larger van dealers have publicly stated that their total Autotrader spend has reached £20,000 a month or more before they started to cut back. Even small changes in stock levels or package tiers can shift a dealer into a higher band with very little notice.

The market rewards this behaviour. Autotrader’s share price has remained strong throughout 2024 and 2025, hovering around 650 to 680p. Investors are benefiting from the rising revenue and record margins. Dealers are the ones funding it.

Independent dealers with around 50 cars regularly report monthly invoices of £3,000 to £4,000. In one well known dealer group a site shared that they pay £3,500 for 50 cars. Larger van dealers have publicly stated that their total Autotrader spend has reached £20,000 a month or more before they started to cut back. Even small changes in stock levels or package tiers can shift a dealer into a higher band with very little notice.

The market rewards this behaviour. Autotrader’s share price has remained strong throughout 2024 and 2025, hovering around 650 to 680p. Investors are benefiting from the rising revenue and record margins. Dealers are the ones funding it.

“Investors are benefiting from the rising revenue and record margins. Dealers are the ones funding it.“

This creates an uncomfortable truth. Autotrader is delivering exceptional results as a business, but it is becoming harder for many dealers to justify the scale of the spend without equivalent gains in lead quantity and quality.

Why So Many Car Dealers Are Now Searching For An Autotrader Alternative

More dealers than ever are actively searching for an Autotrader alternative, and the trend is clear in search data. Keywords like “autotrader alternative” and “sites similar to autotrader” attract hundreds of searches every month. What this tells us is simple. Dealers are no longer just frustrated with rising costs. They are actively exploring options, comparing platforms and looking for ways to take back control over their customer acquisition.

The problem is that most lists of “sites similar to Autotrader” only offer other marketplaces. They do not solve the core issue, which is dependence. Dealers do not need another classified site. They need a way to generate leads directly, own the data, manage the journey and stop relying on a single platform that becomes more expensive every year.

The problem is that most lists of “sites similar to Autotrader” only offer other marketplaces. They do not solve the core issue, which is dependence. Dealers do not need another classified site. They need a way to generate leads directly, own the data, manage the journey and stop relying on a single platform that becomes more expensive every year.

The Problem With Relying on One Marketplace

Using Autotrader is not the issue. Relying on Autotrader almost entirely is. When a large portion of your leads come from one platform (that you don’t own) you effectively rent your customers. You do not control how the user journey works, what information is displayed, how data is collected or how enquiries arrive.

The Deal Builder rollout made this clearer than ever. Sign in became mandatory before an enquiry, reducing lead volume for many dealers. Customer contact methods changed. Parts of the user journey were handled by Autotrader rather than the dealership. Dealers felt like decisions were being made for them rather than with them. Some described it as feeling more like a dictatorship than a customer relationship.

The bigger issue is that this dependence leaves dealers vulnerable. Prices rise each year and you have little negotiating power. Changes to the platform can reduce results without warning. And while you pay more, Autotrader owns the data, not you.

Dealers can and should continue to list on Autotrader. But depending on it for all or most of your demand leaves you really exposed and limits growth.

The Deal Builder rollout made this clearer than ever. Sign in became mandatory before an enquiry, reducing lead volume for many dealers. Customer contact methods changed. Parts of the user journey were handled by Autotrader rather than the dealership. Dealers felt like decisions were being made for them rather than with them. Some described it as feeling more like a dictatorship than a customer relationship.

The bigger issue is that this dependence leaves dealers vulnerable. Prices rise each year and you have little negotiating power. Changes to the platform can reduce results without warning. And while you pay more, Autotrader owns the data, not you.

Dealers can and should continue to list on Autotrader. But depending on it for all or most of your demand leaves you really exposed and limits growth.

Why “Autotrader Alternatives” Are Not The Answer Dealers Think They Are

When someone searches for an Autotrader alternative or for sites similar to Autotrader, what they usually find is a long list of other classified platforms. None of these options deliver the visibility or volume that dealers need, and none of them solve the real issue. Moving from one marketplace to another does not reduce dependency. It simply shifts it.

The only meaningful alternative is not another platform. It is building your own acquisition engine. Your own Search, Demand Gen and YouTube strategy. Your own data, your own leads and your own customer journey. This is the only approach that gives long term efficiency and stability.

The only meaningful alternative is not another platform. It is building your own acquisition engine. Your own Search, Demand Gen and YouTube strategy. Your own data, your own leads and your own customer journey. This is the only approach that gives long term efficiency and stability.

What Your Own Acquisition Engine Looks Like

For dealers with around 30 to 50 cars, the right starting point is usually in the region of £2,000 per month. This gives enough budget to cover strong geographic targeting across Paid Search, Demand Gen and YouTube, while also creating room for retargeting and brand reinforcement.

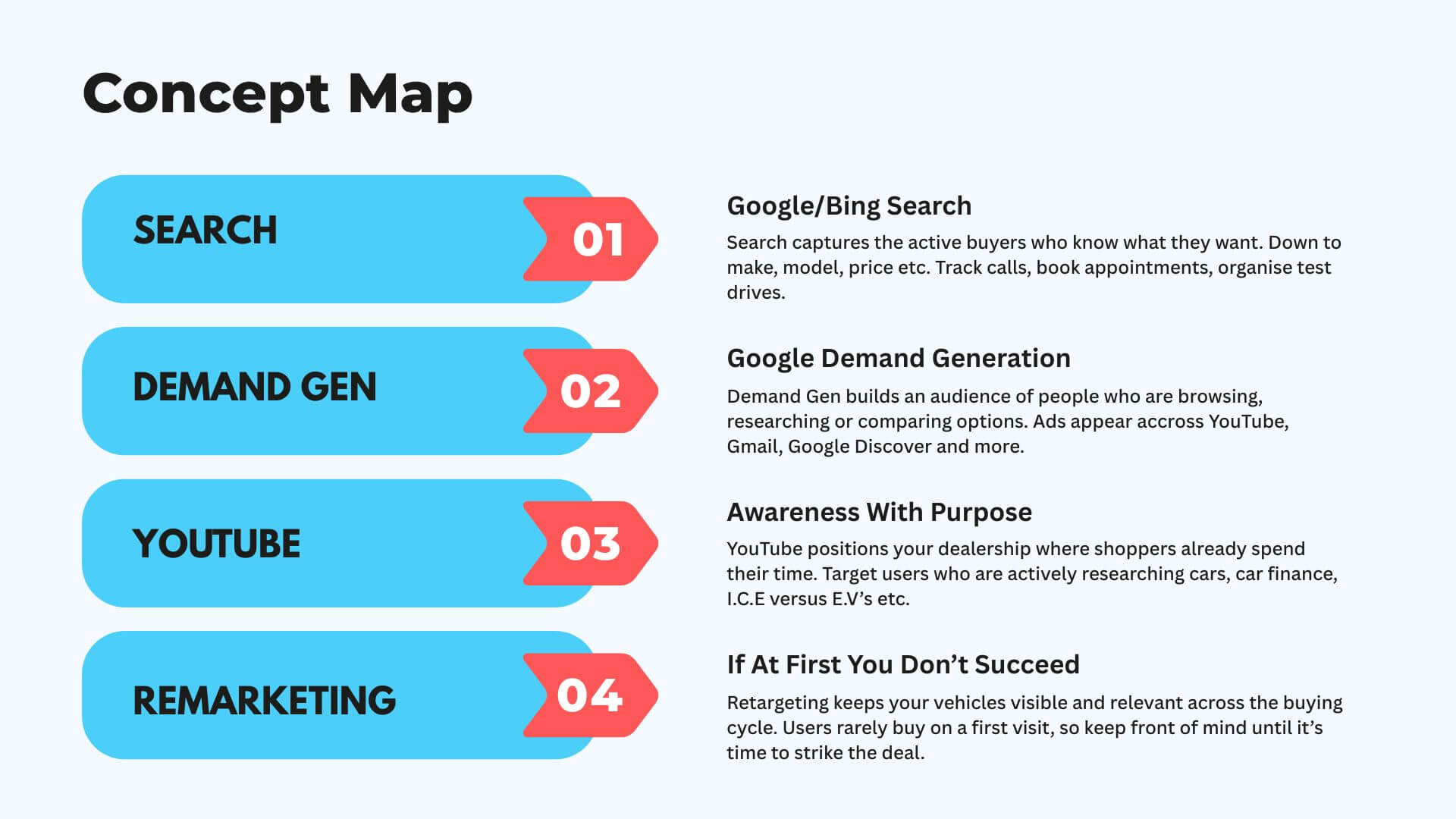

The structure is simple. Search captures the active buyers who know what they want. Demand Gen builds an audience of people who are browsing, researching or comparing options. YouTube positions your dealership where shoppers already spend their time. Retargeting keeps your vehicles visible and relevant across the buying cycle.

The difference is control. When you run your own acquisition engine you decide how leads flow. You decide which models or stock types get more budget. You decide how enquiries are handled and what data is captured. Over time you also build a pipeline of previous visitors who can be converted more efficiently, reducing your cost per sale.

This is the part many dealers do not realise. With Autotrader the cost increases each year. With your own acquisition engine performance improves each year. You get better at finding the right buyers, matching stock to intent and reducing wasted spend. You get more efficient with time.

The structure is simple. Search captures the active buyers who know what they want. Demand Gen builds an audience of people who are browsing, researching or comparing options. YouTube positions your dealership where shoppers already spend their time. Retargeting keeps your vehicles visible and relevant across the buying cycle.

The difference is control. When you run your own acquisition engine you decide how leads flow. You decide which models or stock types get more budget. You decide how enquiries are handled and what data is captured. Over time you also build a pipeline of previous visitors who can be converted more efficiently, reducing your cost per sale.

This is the part many dealers do not realise. With Autotrader the cost increases each year. With your own acquisition engine performance improves each year. You get better at finding the right buyers, matching stock to intent and reducing wasted spend. You get more efficient with time.

The Numbers That Matter

If you are paying more than £3,000 to £4,000 per month to Autotrader, shifting even a portion of that into your own channels delivers immediate value. You are investing in something you own. You are diversifying your demand. You are building an asset instead of renting exposure. Most importantly you are creating a predictable, controlled and measurable engine that improves every month rather than becoming more expensive.

Our experience shows that once dealers start running their own acquisition, three things happen very quickly. Their waste drops. Their lead quality increases. Their dependency on Autotrader falls. The result is a more resilient and efficient business that has far more control over cost per lead and cost per sale.

Our experience shows that once dealers start running their own acquisition, three things happen very quickly. Their waste drops. Their lead quality increases. Their dependency on Autotrader falls. The result is a more resilient and efficient business that has far more control over cost per lead and cost per sale.

How Precisionly Helps Dealers Take Back Control

Precisionly works with independent dealers and groups that want to reduce waste and build a sustainable acquisition engine. The focus is always on efficiency and measurable outcomes. We combine Paid Search, Demand Gen, YouTube and retargeting to create full coverage across the buyer journey.

For dealers with 30 to 50+ cars the goal is simple. Build a high performing acquisition system that works alongside Autotrader rather than beneath it. For larger dealers the aim is to scale this across multiple locations, keeping spend tight and performance transparent.

Everything is built around clean measurement, lead quality and clarity. No long contracts. No jargon. No surprises. Just precision-led customer acquisition that gives you more control over your business.

For dealers with 30 to 50+ cars the goal is simple. Build a high performing acquisition system that works alongside Autotrader rather than beneath it. For larger dealers the aim is to scale this across multiple locations, keeping spend tight and performance transparent.

Everything is built around clean measurement, lead quality and clarity. No long contracts. No jargon. No surprises. Just precision-led customer acquisition that gives you more control over your business.

Final Thoughts

Autotrader remains the dominant marketplace, but it should not be your entire strategy. The rise in searches for “autotrader alternative” and “sites similar to autotrader” shows that dealers are already looking for ways to rebalance their approach. Building your own acquisition engine is the most effective and sustainable way to do that.

If you would like to explore what this could look like for your dealership, Precisionly offers a no pressure conversation and a detailed opportunity report for your stock level and area. It is the quickest way to see how much control and efficiency you can win back.

Control your ad spend, own the data exclusively that comes from that investment, build a system that’s transparent and drive your business forward.

Run smarter. Scale faster. Build demand you own.

If you would like to explore what this could look like for your dealership, Precisionly offers a no pressure conversation and a detailed opportunity report for your stock level and area. It is the quickest way to see how much control and efficiency you can win back.

Control your ad spend, own the data exclusively that comes from that investment, build a system that’s transparent and drive your business forward.

Run smarter. Scale faster. Build demand you own.

Need help turning this into real-world performance?